Reverse Factoring

In a gloomy economic climate and an increasingly restrictive regulatory context (LME [French Law on the Modernisation of the Economy], Basel III, etc.), banks are increasingly wary when it comes to financing companies, at a time when cash flows are feeling the pinch. In these uncertain times, CFOs are searching more than ever for ways to improve performance.

Reverse factoring is a financing solution that remains underused, despite its numerous advantages. It enables the company to:

- capture some of the income from suppliers’ expected payments

- reinforce Working Capital Requirement, within certain limits.

Reverse factoring thus strikes two chords to which every company is attuned: increasing profitability and reducing capital employed. It also offers a powerful tool for Financial and Purchasing divisions to optimise return on capital employed (ROCE).

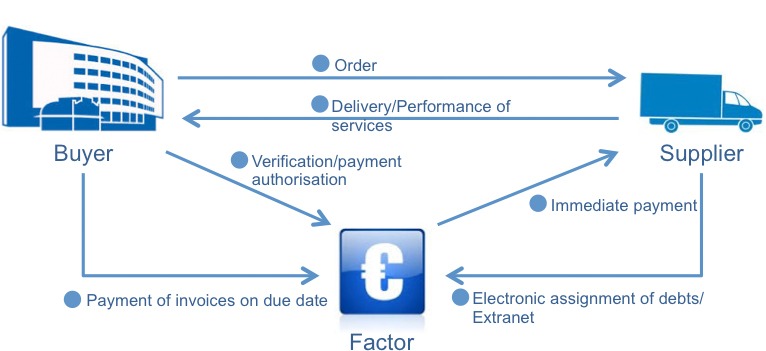

How does reverse factoring work?

- Company X signs a partnership agreement with a factor, while its supplier signs a simplified factoring contract with the same factor.

- The supplier sends its invoices to the factor and company X simultaneously.

- As soon as it receives the firm and irrevocable authorisation to pay, the factor settles the invoice with the supplier by bank transfer and debits company X on the invoice due date.

What are the advantages of reverse factoring?

- Increased margin: if the supplier is paid promptly, company X can negotiate a discount under favourable terms covering at least the cost of the interest and expenses inherent to the reverse factoring service.

- Stable, even improved, cash flow and WCR: the situation is the same as if company X paid its invoices at their due date; it is even possible, under certain conditions, to occasionally compensate for the restrictions imposed by the LME by negotiating with the factor to reimburse advances paid by the latter more than 60 days later, etc.

- Reduced administrative costs: company X only has to pay one service provider at predetermined intervals (week, decade, month, etc.). This process also enables the cash manager to control cash flow more effectively.

- Increased loyalty with respect to strategic suppliers, which can prove useful in the long term

What are the advantages for suppliers?

- A new source of financing by prompt payment of a proportion of their sales

- Improved cash flow and the possibility to deconsolidate their receivables

- Credit risk coverage for a strategic client (transfer of the client risk to a financial institution)

- Simplification of client follow-up

What are the prerequisites for reverse factoring?

- Company X must have a good rating with credit insurers

Fundamental prerequisite: in order for this operation to be set up and remain viable over time, company X must have a good rating with credit insurers as it is the factor which takes on the credit risk, for high unit amounts.

- Good communications and a computer interface between the factor and company X

In order to enable the factor to offer suppliers attractive rates, it must incur as few administrative costs as possible.

Similarly, this operation must enable company X to make substantial administrative savings.

It is therefore necessary to have fully automated links and validation procedures between company X and the factor:

- validation of orders, delivery notes, invoices, etc.

- fully automated payments by company X with detailed breakdown,

- mutual verification of payments and withdrawals (factor / client) enabling automatic reconciliation, etc.

What are the costs associated with reverse factoring?

Factor charges

- A service commission called a “factoring commission”

- A financing commission

- Various management fees

Conclusion

Reverse Factoring has evolved and is now:

- accessible to a greater number of companies (medium-sized, number of suppliers)

- more attractive financially

This mechanism offers:

- more autonomy compared to traditional sources of bank financing

- a secure supply chain

The programme must be customised according to the economic and financial situation of the company, its objectives, the number of suppliers, their trade sectors and the volume of outstanding accounts.